Senin, 03 Februari 2020 | 1086 kali

Muhammmad Meirizky Ikhsan, S.E., M.P.A.,

(Pelaksana Kantor Pelayanan Kekayaan Negara dan Lelang

Palembang, Direktorat Jenderal Kekayaan Negara, Kementerian Keuangan RI, 2020)

meirizky@kemenkeu.go.id

A. Introduction

The last feature of the Financial

Report of Central Government (LKPP) stated that Indonesia’s fixed assets were

amounted to IDR 1,931 trillion or 28% of total assets (BPK 2018a). Those amounts

do not include value of revaluation program commencing in 2017 – 2018 with the

potential increase to IDR 5,728 trillion which was more than 200% increase from

its initial value (BPK 2018b). Nevertheless, The Financial Audit Agency (BPK)

could not accept the fair value generated by revaluation program due to the

several issues.

According to BPK’s audit report on

the program, the problems can be divided into two responsibilities, which were assets

inventory on Asset Users (K/L) side and valuation on the Assets Manager,

Directorate General of State Assets Management (DJKN). As the recent

revaluation program uses the new method of Desktop Valuation (measuring fair

value without field checking), the quality of assets inventory conducted by Assets

Users was closely related to the quality of fair value produced. It becomes an

issue because such program was not the first attempt in measuring fair value of

Indonesia’s state-owned assets.

It was firstly commenced in 2007 –

2010 namely Inventory and Valuation (IP) program, then about ten years later

the second IP (revaluation) program were conducted. Nevertheless, the 2017 –

2018 revaluation program has revealed vast number of unrecorded assets, which

are then recorded as excessive assets, as well as missing assets. Generally,

the BPK’s findings affirmed that the recorded assets were not in accordance

with the factual conditions including specification, quality and quantity.

Although policy instruments have been issued by DJKN to bond Asset Users’

concerning assets management responsibilities, it shows that the assets inventory

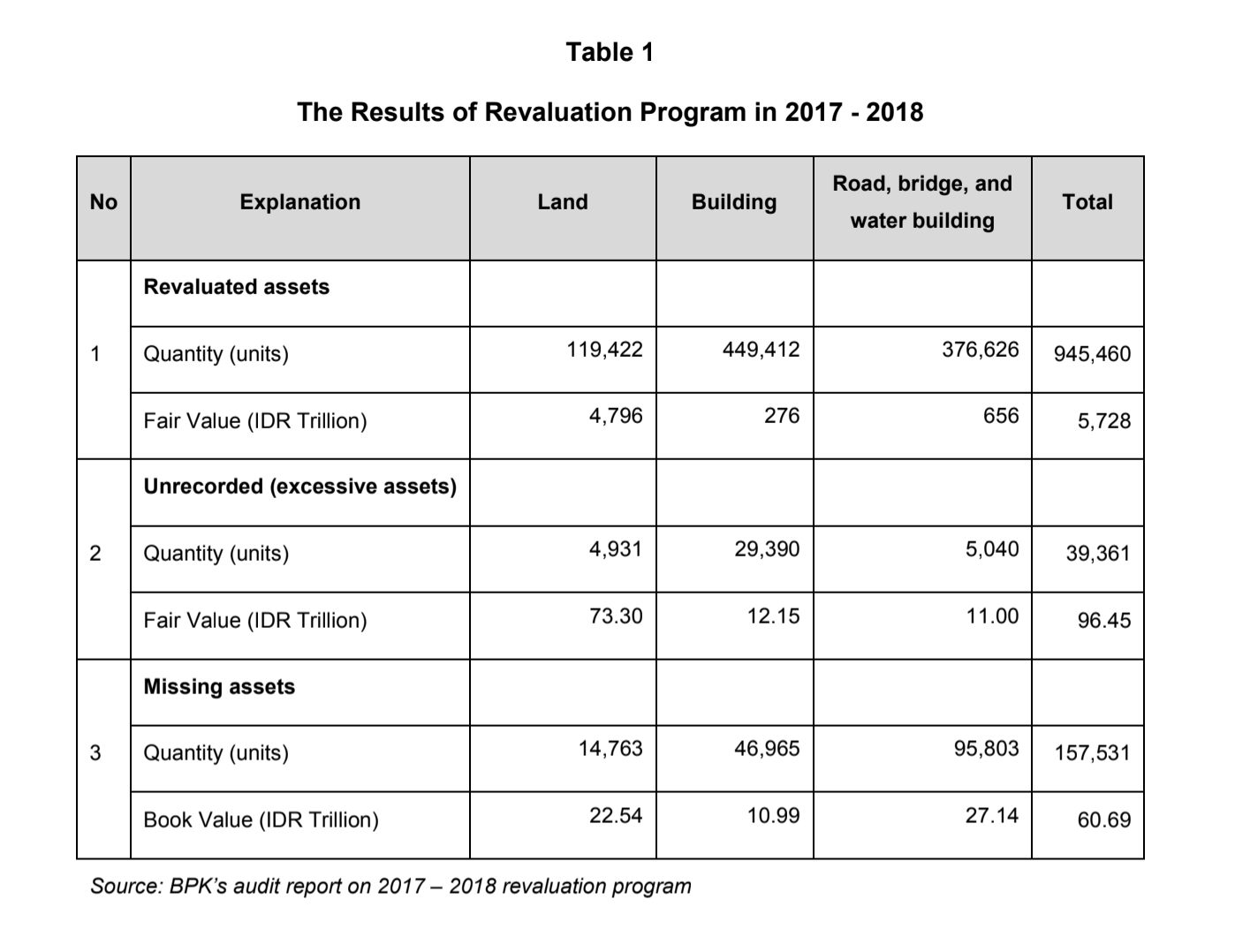

on the Assets Users is still problematic. The following table shows the amount

of unrecorded and missing assets resulted from the revaluation program.

The low quality assets inventory will

not only affect the revaluation program, but further assets management process

and the audit opinion on LKPP. Beside its negative effects on public

accountability, the absence of good assets inventory system will limit options

for assets optimization. Consequently, the DJKN’s vision of Revenue Center as

well as Distinguished Assets Manager will be a long and windy road. This paper

will assess the characteristics of wicked problem that might be attached with

assets inventory problems. Then improved assets’ database and continuous

communication about assets management issues are proposed actions that need to

be considered to address wicked problem in assets management field.

To

have a focused discussion in achieving the objectives, this paper assumes that

state-owned assets consist of land, building, road, bridge, and water building.

1. Defining

Wicked Problem

Wicked problem is different from the

common policy problem which can be solved by relatively simple policy planning as

wicked problem is featured by complexity, uncertainty, and divergence of

problem (Head 2008, p. 103). Meanwhile, Newman and Head (2017, p. 41) suggested that the wicked

problem is not simply defined as “problems

that are complicated or difficult to solve”, but they mentioned factors that

cause the wickedness which “impede problem definition, hinder stakeholder

agreement, interfere with the selection of appropriate approaches or solutions,

and create unbounded and unmanageable negative externalities”. Therefore, if policy

makers find difficulties to mention the entire possible root causes of a policy

issue and the existence of uncontrollable approaches-consequences, it is one

indication that they are facing a wicked problem.

2. The

Consequences of wicked

problem

In public policy, improper approach

in addressing certain policy issues will create another policy problem/s. For

instance, the recent revaluation program has unintentionally slowed the public

services delivery of DJKN, especially in process of assets management approval.

On the other hand, if the BPK’s findings of the revaluation program are not

corrected, it will deteriorate public trust on the government. However, in the

end of 2019, BPK seems ‘softened’ by DJKN’s solid efforts in making significant

improvement so that revaluation result could be included in the Financial

Report of Central Government year 2019.

This shows that policy planning is

critical to minimize the drawbacks of policy implementation. As the relatively

easy policy problems could be responded with the rigorous identifications of

possible approaches in particular situations, wicked problems involve complex

process both in identifying policy problems and finding alternative solution to

resolve the problems. Many researches put climate change and poverty as real

example of wicked problem. Thus, reducing poverty level can be a multi-complex

discussion among policy makers due to various attributes around the issues and

the solutions may generate biased outcomes. It is similar with the policy on

addressing climate change, as nature cannot be predicted and so many actors

that need to be involved together to dicuss it with uncertainty of results of

the chosen alternatives. As for wicked problems, it seems that there is no clear

solution in both identifying and addressing the problems.

In the topic of assets inventory,

responsibility of inventorization is on the Assets Users. However, the

consequences of lack of due diligence of that responsibility will affect not

only the Assets Users but also the Assets Manager as the information given

around that assets reports are not valid. Moreover, regulatory body does not

have full capability to insist Assets Users to comply with the regulations.

Different values and organizational structures, lack of public officials’

concern and understanding, and limited internal control are some of many other

complex possible causes of stagnant assets inventory quality within the Assets Users.

Those factors have not considered some possible issues on the Asset Managers.

In wicked problems, everything seems related and multi-complex.

C. Discussion

1. Is

asset inventory that wicked so

then it could be called wicked problem?

During the New Order regime, Indonesian government was entering the

period of assets administration when assets inventory was conducted manually

(Hadiyanto 2009). Meanwhile, the state assets reforms have been started since

2006 noted with the establishment of Directorate General of State Assets (DJKN).

Around a year later, Indonesian government pioneered the State-owned Assets Inventory

and Valuation (IP) program which claimed the first fixed assets account with

the amount of IDR 410 trillion (BPK 2010). Then, in 2017 – 2018, government

rolled the second phase of State-owned Assets Inventory and Valuation (Revaluation)

program. Albeit DJKN has made efforts to mitigate risks of the program, the

result of BPK’s audit showed that the efforts have not been approved as

effective. One of the BPK’s findings (2018c) claimed that the incomplete

information and invalid data from assets inventory has caused inaccurate result

of revaluation program.

Responding to BPK’s recommendation on

assets inventory issues, Ministry of Finance through DJKN exerts the Asset Users

to comprehensively improve their assets inventory. Accordingly, in 2019, assets

which were included in BPK’s findings and have significant value, were

reinvented and revalued. However, it can be argued that such actions engaged only

to respond on the BPK’s recommendation but did not constructively identify and

address the root causes of lack assets inventory quality in the Assets Users.

It is fully understood that the limited time given has put government came up

into the most priority issues which is responding to BPK’s suggestions so that

all the released revaluation 2017 – 2018 efforts were not wasted. However,

government needs to consider how the assets inventory issues are going to be

resolved comprehensively.

The assets inventory plays

significant role in assets life cycle. As In the Government Law Number 27 of 2014,

it is categorized under the assets administration phase along with assets

recording and reporting. Realizing the critical role of this phase, Ministry of

Finance through the Minister of Finance Regulation Number 244/PMK.06/2012

emphasizes more the obligation of Asset Users related to assets administration,

including assets inventory. This regulation has begun to include the role of Government

Internal Supervisory Apparatus (APIP) to ensure that the assets inventory obligation is

carried out according to the applicable regulations. To strengthen this phase,

government issued Minister of Finance Regulation Number 181/PMK.06/2016 that

provides technical guidance of assets inventory. It also introduced new level of punishment for

those who do not comply. This series of regulations implies that DJKN, as

policy maker of state-owned assets, has taken into account the significance of

assets inventory in

asset management. Nevertheless, the recent audit’s findings have unveiled that Asset

Users are not implemented the regulations adequately.

The fact that policies on

assets inventory are

unable to solely assist government to have a quality revaluation program is one

indication of the uncertainty of policy outcomes. Rittel and Webber (1973)

mentioned that “decision making under deep uncertainty is a particular type of

wicked problem”. On the other hand, based on Law Number 1 of 2004,

responsibility of assets inventory is on the Assets Users which are

ministries/agencies. However, in the audit reports on LKPP (2009 – 2018), BPK

declared that ministries/agencies’ internal control system on inventories and

fixed-assets are inadequate which causes incompliance towards the applicable

regulations and inaccuracy of assets’ information. Meanwhile,

ministries/agencies, with their diverse primary duties, organizational culture,

and resources, might create various perceptions about assets management.

Accordingly, as noted before, unclear policy outcomes, complex attributes of

the problem, and the involvement of many actors (ministers/agencies), are more

than enough to consider assets inventory as wicked problem, especially in the field of

assets management.

2.

Policy on assets

management will be less effective due to issues on assets inventory

Assets management reform

started in 2007 which has shifted the management assets mindset from assets administrators

to assets manager (Mardiasmo 2012). Before the reform, public organization

focused on how to build and purchase assets, therefore, with the new paradigm,

state-owned assets discussions have transformed to topic about how assets can

be utilized optimally and generate additional revenues. Likewise Minister of

Finance (Media Indonesia 2019) stated that assets should be utilized at its

optimum level for people’s prosperity. She said that assets need to be awakened

from their ‘long sleep’. In accordance with that, DJKN (2019a) has launched its

Roadmap of 2019 – 2028, with the vision of being ‘a distinguished asset

manager’ that would realize one of its mission to become Revenue Center.

However, DJKN (2019a) has

recognized that more than 80% assets are under the authority of other

ministries/agencies. Ideally, to achieve an ultimate condition of assets

management, DJKN as Assets Manager, and ministers/agencies as Assets Users,

need to sing in same rhythm. Nevertheless, it is not as easy as it sounds.

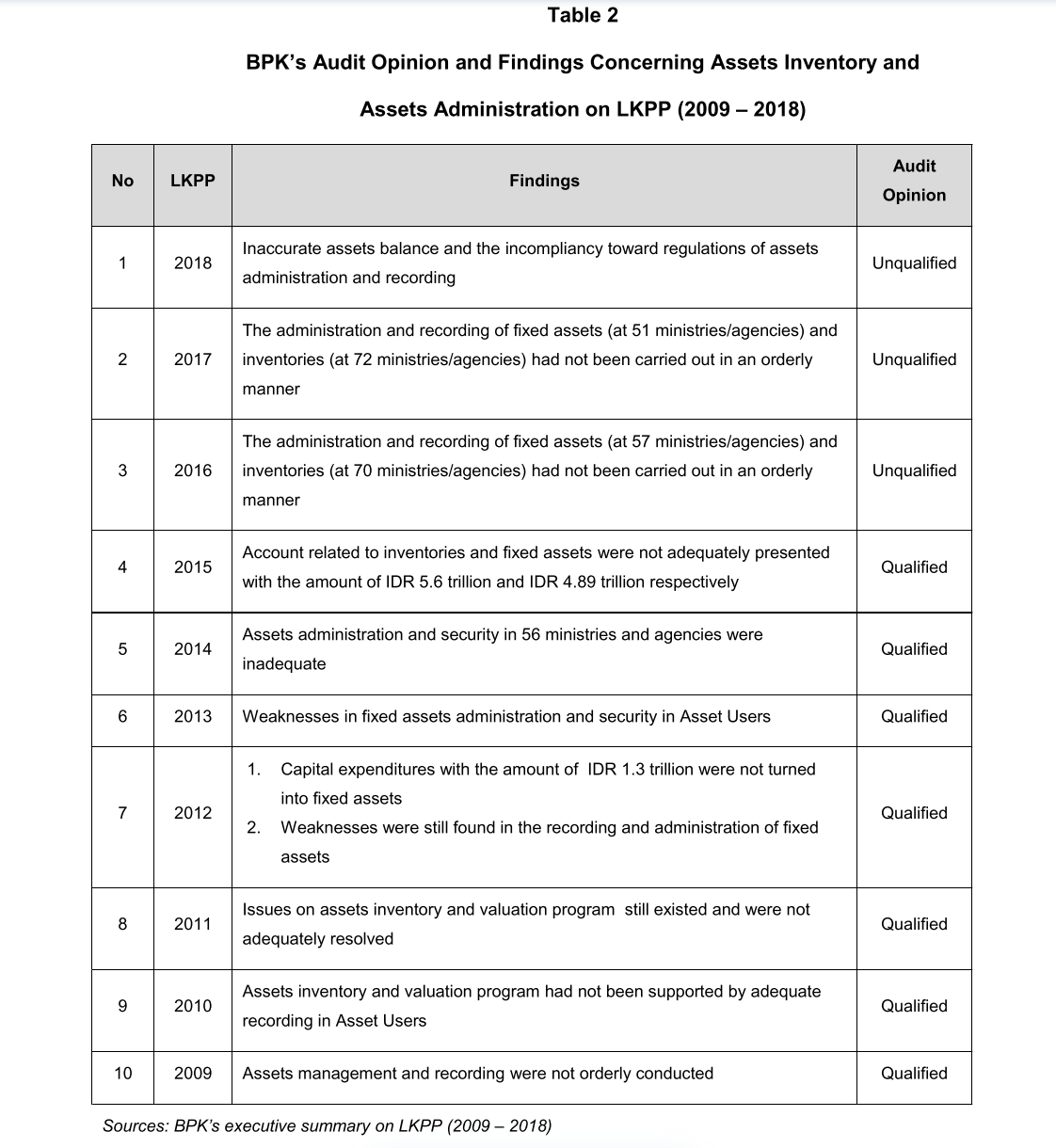

BPK’s reports (2009 – 2018) have shown that assets administration performance

within ministries/agencies have not shown satisfying results. Table 2 shows

BPK’s findings related to assets inventory and administration (2009 – 2018).

The figures explain that

assets inventory issues

have been repeatedly found during the last decade. It seems that policy

instruments are insignificant in addressing the assets inventory problems.

Although recent LKPP’s opinion has been satisfying compared to a decade ago,

the problem around assets inventory still exists. Even in advanced countries,

the need of improvements is highly regarded, and the assets inventory and record are

considered as basic requirements for a complex field of assets management

(Mardiasmo 2012). Therefore, the role of DJKN is critical to assure the

development of assets management policies so our basic needs of the valid and

accurate information of assets are available for further asset management. Just

like property agents, even though they are not the owner, based in the accurate

and comprehensive information of property given by the owner, they can ‘utilize’

(sale) the property to the ‘suitable’ buyer (generating optimal income/revenue).

Therefore if the assets inventory cannot produce high quality assets’ information

(condition, location, quantity, specification, etc.), it can be argued that

assets management policies would not be effective.

|

|

3. What can government do about it?

a. Rethinking about quality assets database

As assets management reforms have

shifted the assets management paradigm from ‘assets administrator’ to ‘assets

manager’, the quality assets database is inevitable condition. It seems that

government needs to realize that there are weaknesses in the current assets inventory

framework in achieving policy outcome of creating distinctive assets database.

Therefore, it needs to assess whether the drawbacks is on policy making, policy

implementation, or policy evaluation stage.

BPK reports can be used as an evaluation

tool to assess whether particular policy can effectively meet the expected

policy outcome. There are, at least, three recommendations for resolving the

problems suggested by BPK (2017), which are:

1)

to conduct assets tracing and improvement of assets

application

2)

to improve the implementation assets administration

control

3)

to carry out control and supervision of assets.

However, since the recent policies

regarding assets inventory were released, which are Minister of Finance

Regulation Number 181/PMK.06/2016 and Number 52/PMK.06/2016, BPK’s findings on

assets inventory were not enhanced significantly. This might have negative

effects on public accountability and public services delivery.

Government accountability might be

questionable as information of assets is not presented concerning their factual

conditions. Public questions possibly will expand to other public financial and

practices responsibilities. For instance, if there is a huge budget allocated

to certain infrastructure program, people need to be assured that spending is

transformed into physical assets. Without the proper assets inventory, those

assets might not be recorded according to its real value. Thus, public trust

towards government might decrease. Therefore, it is evident that assets administration

is considered as an accountability tool.

On the other hand, the absence of

valid and accurate assets information, might lead to deteriorated quality of

public services. Meanwhile, one main objective of government spending is to

maintain high level of public services delivery. However, without reliable data

on assets quality and quantity, budget allocation for enhancing public services

delivery might not generate significant outcome as purchased or constructed

assets could not meet the real public organizations’ needs. For example,

whenever a public organizations do not regularly update technical condition of

its building (whether it is light or severe damage), the allocated budget for

maintaining the building might not be optimal.

Consequently, the decreasing quality of building caused by poor planning

will reduce the useful life time of assets used for public services delivery.

Therefore, it is evident that the quality of asset database is an important

issue for government for a better assets management system.

b. Enhancing communication of the importance of assets management

to ministries/agencies as Asset Users

Communication is a core of any

relationship. It includes coordination, socialization, collaboration, and any

form of communicating the significance of implementing states asset management.

Even a simple message if not communicated correctly will not achieve its

initial intentions. Actors related with the matter need to understand each

obligation and responsibility, therefore, they could generate a fruitful

communication. Meanwhile, Conklin (2006) argued that with wicked problem, the

policy decision is not to solve the problem but more like to initiate coherent

action among stakeholders. By communicating assets management issues, what we

expect is not only to adapt collaborative actions in policy making process but

to enhance the understandability and the sense of awareness about the

importance of compliancy towards regulations with states assets management.

The diversity of public services or

duties among public organization adds to the complexity of finding the

alternative solutions of ideal states assets inventory. Apart from the varied

public organizations’ function, it is evident that disparity of public

managers’ attention between public finance and public assets still exists.

Additionally, Minister of Finance (Bisnis Indonesia 2020) argued that

unsynchronized data on capital expenditure planning with assets report shows

that there is no coherent perception between Budget Users in public

organizations and their stakeholders. For instance, although Indonesian

National Army and Ministry of Defense’s main duty is national defense, they

have to manage their assets according to applicable regulations because the

existence of public services must be in line with good assets management as

part of public transparency and accountability.

However, Ministry of Defense’s audit

opinions in 2016 – 2017 were declared ‘qualified’ due to repeated findings

related to assets, despite it significantly records 22% of total Indonesia’s

fixed assets (BPK 2018d). Moreover, in Table 2, it might be argued that for ten

years public organizations have not been able to ‘anticipate’ auditors’

assessment on their assets management practices although some of the findings

are repeated and interrelated on assets. There are two issues which may cause

that phenomenon.

1) Firstly, it seems that public organizations are not

having sense of necessity and urgency in performing assets management

practices. Accordingly, public managers are faced with various targets, assignments,

and programs related to their public duties, which might divert their focus on

obligation of states assets management. Hence, it is critical to communicate

the awareness of assets management obligation to public managers in the

ministries/agencies to keep them maintaining sustainable assets management

conducts.

2) Secondly, resources, including fund, expertise, time,

and knowledge, are limited to execute good assets management in recent more dynamic

and multifaceted public services delivery. Unfortunately, the improving role of

government in the provision of public services is not always accompanied by

increasing resources which consequently will reduce resources for implementing

decent assets management. Therefore, with communication, policy makers might

reveal the implementation problems between public officials and public managers

or Assets Users and Assets Manager, thus, policy maker can evaluate and improve

the policy making process to resolve the issues.

Subsequently, it can be argued that

communication is needed to be stretched-out not only across ministries/agencies

(Assets Users and Assets Manager) but also within ministries/agencies (public managers

and public officials) about the importance of assets management.

c. Communication channels in promoting state assets

management policies

As Asset Manager, DJKN has

prominent role in assuring that ‘information’ and ‘knowledge’ about assets

management policies are inherently acquired and implemented by assets

stakeholders including ministries/agencies as Assets Users, Government

Internal Supervisory Apparatuses, local governments, and other third parties (such as

grant givers, renters, utilization partners, etc.). Continuous communication

can be conducted through various channels like regular workshops, short courses,

electronic and social media exposures, and more importantly, supervisory and

control visitation by assets users. In one of its publications, Australian

Public Services Commission (2018) suggested that “sustained behavioral change

by many stakeholders and/or citizens” is part of solutions to address wicked

problem. Therefore, DJKN needs to develop the way of communicating its

policies, including assets management issues, to its stakeholders for them to

induce the sense urgency and necessity of performing outstanding assets

management. This will also be linier with one of government assets management

reforms vision which is to stimulate behavioral change associated with state

assets management from administrating (maintenance and/or administrative oriented)

to managing (optimizing oriented).

Moreover, workshops and short

courses are critical to build relevant understanding and competency for all

level of public officials, because it is going to be more optimal if both Assets

Users and Asset Manager are having equal perception in managing state assets.

Accordingly, although Assets Users are obliged to check and balance their

assets management mechanism (PMK 244/PMK.06/2016), the field supervisory visits

from assets manager are needed to communicate, coordinate, and evaluate

specifically as well as directly about their performance on assets management (DJKN

2019b). This could be illustrated like when an assets manager might consider

that allocated fund for communicate its company or services is a form of ‘advertisement’

which turns out to be investment instead of cost to fuel its asset performance.

On the other hand, public organizations need to realize that there is no

short-cut to resolve wicked problems; however “a broad recognition and understanding,

including government and Ministries” is one critical condition for resolving

wicked problem in assets inventory (APSC 2018). Consequently, it is critical

for DJKN to ‘invest’ adequate budget for funding those programs and activities

which will contribute positively to DJKN’s achievements both in quality assets’

database and significant non-tax revenue from assets management.

D. Conclusion

To sum up, the assets inventory

issue in Indonesian public organizations seems to meet some, if not all,

categories of wicked problem. To argue about the wickedness problem of assets inventory,

one can basically understand about reasons why BPK, in the last decade of its

audit reports and recent revaluation program, noted that asset inventory has

not been performed with adequate confidence to meet accountability aspects. On

the other hand, the recent Minister of Finance’s comment (Bisnis Indonesia 2020)

has admitted that some ministries have not orderly managed public funds

allocated to their ministries; one example is non-uniformity between capital expenditures

allocation and records on assets addition in the end of year. Thus, Ministry of

Finance, through DJKN, has become champ of assets management reform by issuing

some of policies in assets inventory, such as Minister of Finance Regulation Number

244/PMK.06/2012, 181/PMK.06/2016, 52/PMK.06/2016, and 118/PMK.06/2017, however,

policies implementation seem has not been showing satisfying results. This news

might also somehow affect the DJKN’s next projects in assets management which

are namely assets insurance, assets optimization, assets portfolio evaluation,

and more notably, new capital city (IKN).

Quality assets’ database and

continuous communication are among factors that are arguably significant in

taming, if not resolving, wickedness of assets inventory issues. It is evident

that the availability of valid data on assets is one of public accountability

and transparency prerequisite. If government wants to be held accountable by

public, then the accurate data of how it manages public money, including

assets, should be on its priority list. However, the suboptimal policy

implementation on assets inventory has been alleged as contributing factor of

the recent BPK’s audits finding on assets. The lack of public officials’

understanding and attention toward assets management issues, especially within Assets

Users, are one aspect that needs to be considered by policy makers. Therefore,

it is necessary for DJKN, as policy maker, to improve the communication channels

by accommodating regular workshops, short courses, electronic and social media

exposures, and supervisory and control visitation by Assets Users. These

communication tools inevitably play critical roles as ‘investment’ in the whole

assets management framework which, in later time, will contribute to a better

quality assets database and stimulate positive behavioral change of assets

users’ concerning on assets management,

specially assets inventory issues.

Australian Public Service

Commission (APSC), (2018). Tackling wicked problems: A public policy perspective.

[online] Available at: https://www.apsc.gov.au/tackling-wicked-problems-public-policy-perspective (accessed on January 24th 2020)

Bisnis Indonesia,

(2020). Menkeu Sebut Barang Tak Jelas

Senilai Rp63 Triliun, Apa Itu?. [online] Available at: https://ekonomi.bisnis.com/read/20200124/10/1193637/menkeu-sebut-barang-tak-jelas-senilai-rp63-triliun-apa-itu (accessed on January 24th 2020)

Badan Pemeriksa Keuangan (BPK), (2018a). Warta Pemeriksa: Edisi 11 Vol. I – November - 2018. Jakarta: BPK.

Badan Pemeriksa Keuangan (BPK), (2018b). Laporan Hasil Pemeriksaan BPK RI atas Laporan Keuangan Pemerintah Pusat

Tahun 2018. Jakarta: BPK

Badan Pemeriksa Keuangan (BPK), (2018c). Laporan Hasil Pemeriksaan atas Penilaian Barang Milik Negara Tahun 2017

– 2018 pada Kementerian/Lembaga selaku Pengguna Barang, dan Instansi Terkait

Lainnya. Jakarta: BPK

Badan Pemeriksa Keuangan (BPK), (2018d). Pendapat BPK tentang Pelaksanaan dan Pertanggungjawaban Anggaran

Belanja pada Kementerian Pertahanan dan TNI. Jakarta: BPK

Badan Pemeriksa Keuangan (BPK), (2017). Laporan Hasil Pemeriksaan BPK RI atas

Laporan Keuangan Pemerintah Pusat Tahun 2017. Jakarta: BPK

Badan Pemeriksa Keuangan (BPK), (2010). Laporan Hasil Pemeriksaan BPK RI atas

Laporan Keuangan Pemerintah Pusat Tahun 2010. Jakarta: BPK

Conklin, J., (2006). Wicked Problems and Social

Complexity. In Dialogue Mapping: Building Understanding of

Wicked Problems. Chichester: John Wiley.

Direktorat Jenderal

Kekayaan Negara (DJKN),

(2019a). Road Map Direktorat Jenderal Kekayaan Negara 2019 – 2028.

Jakarta: Sekretariat DJKN

Direktorat Jenderal

Kekayaan Negara (DJKN), (2019b). Portal DJKN: Pemantauan Pemanfaatan BMN oleh Itjen Kemenkeu dan KPKNL

Jakarta V di Lokasi Padang Golf Cilangkap, Mabes TNI. Available at: https://www.djkn.kemenkeu.go.id/kpknl-jakarta5/baca-berita/19148/Pemantauan-Pemanfaatan-BMN-oleh-Itjen-Kemenkeu-dan-KPKNL-Jakarta-V-di-Lokasi-Padang-Golf-Cilangkap-Mabes-TNI.html (accessed on January 21st 2020)

Hadiyanto. (2009). Strategic Asset Management: Kontribusi

Pengelolaan Aset Negara Dalam Mewujudkan APBN yang Efektif dan Optimal. Jakarta: DJKN

Head, Brian W., (2008). Wicked Problems in Public Policy. Public

Policy 3(2): 101-118.

Kementerian Keuangan, (2012). Peraturan Menteri Keuangan (PMK) Nomor 244/PMK.06/2012 tentang

Pengawasan dan Pengendalian Barang Milik Negara. Jakarta: Sekretariat Jenderal

Kementerian Keuangan

Kementerian Keuangan, (2016). PMK Nomor 52/PMK.06/2016

tentang Perubahan PMK Nomor 244/PMK.06/2012

tentang Pengawasan dan Pengendalian Barang Milik Negara. Sekretariat Jenderal

Kementerian Keuangan

Kementerian Keuangan, (2016). PMK Nomor 181/PMK.06/2016

tentang Penatausahaan Barang Milik Negara. Jakarta: Sekretariat Jenderal

Kementerian Keuangan

Kementerian Keuangan, (2017). PMK Nomor 118/PMK.06/2016

tentang Pedoman Pelaksanaan Penilaian Kembali Barang Milik Negara. Jakarta: Sekretariat Jenderal

Kementerian Keuangan

Mardiasmo, D., (2012). State

Asset Management Reform in Indonesia: A Wicked Problem (Doctoral

dissertation, Queensland University of Technology).

Media Indonesia, (2019). Menkeu: Pengelolaan Aset Negara Masih Buruk.

[online] Available at: https://mediaindonesia.com/read/detail/268277-menkeu-pengelolaan-aset-negara-masih-buruk (accessed on January 20th 2020)

Newman, Joshua and Brian Head, (2016). The National Context of Wicked Problems:

Comparing Policies on Gun Violence in the US, Canada, and Australia.

Journal of Comparative Policy Analysis: Research and Practice DOI:

10.1080/13876988.2015.1029334

Pemerintah Republik Indonesia, (2004). Undang-undang Nomor 1 Tahun 2003 tentang

Perbendaharaan Negara. Jakarta: Sekretariat Negara

Pemerintah Republik Indonesia, (2014). Peraturan Pemerintah Nomor 27 Tahun 2014

tentang Pengelolaan Barang Milik Negara/Daerah. Jakarta: Sekretariat Negara

Rittel, H.W. J. and

Webber, M.M. (1973). Dilemmas in a

General Theory of Planning, Policy Sciences. 4

(2): 155-169